GDP Growth And Stock Market Return Correlates Less Than You Think

How Should Investors Allocate To Avoid Home Country Bias?

Investors tend to invest in their familiar asset classes and securities. We call that the home country bias, or invest in your own backyard. There’s nothing wrong with investing in your own backyard; however, for asset allocation purposes, it implicitly underweights the unfamiliars and overweights the familiars.

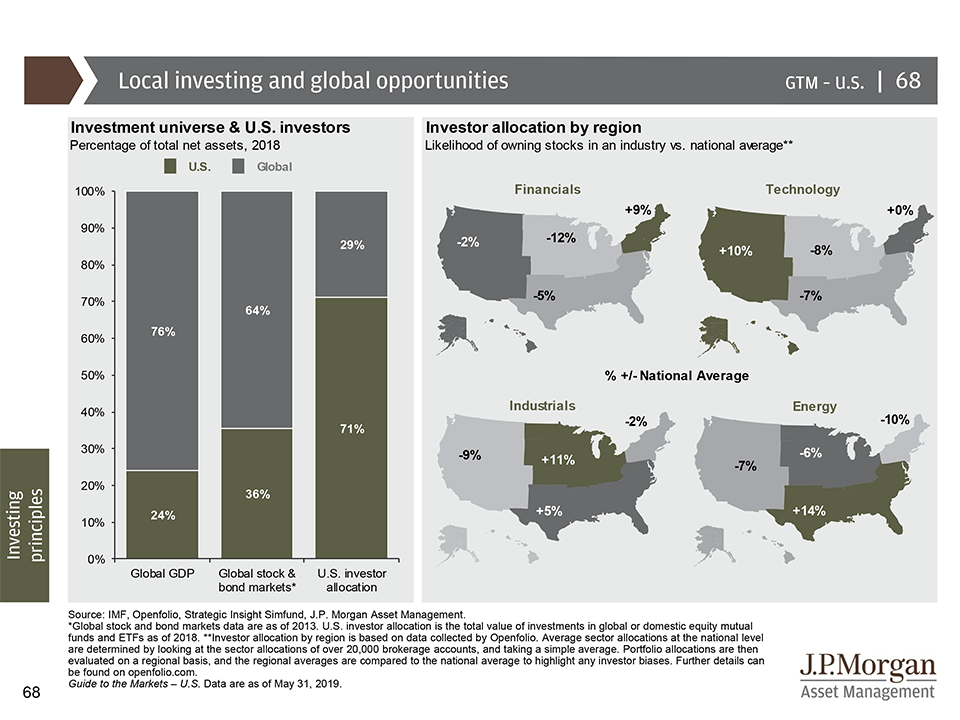

Here we have a slide from JP Morgan to demonstrate investor allocations by US regions and US as a whole. Not surprisingly, West Coast investors tend to overweight tech. Across the US, investors tend to overweight holding US equities even while the rest of the world are providing much of the GDP growth.

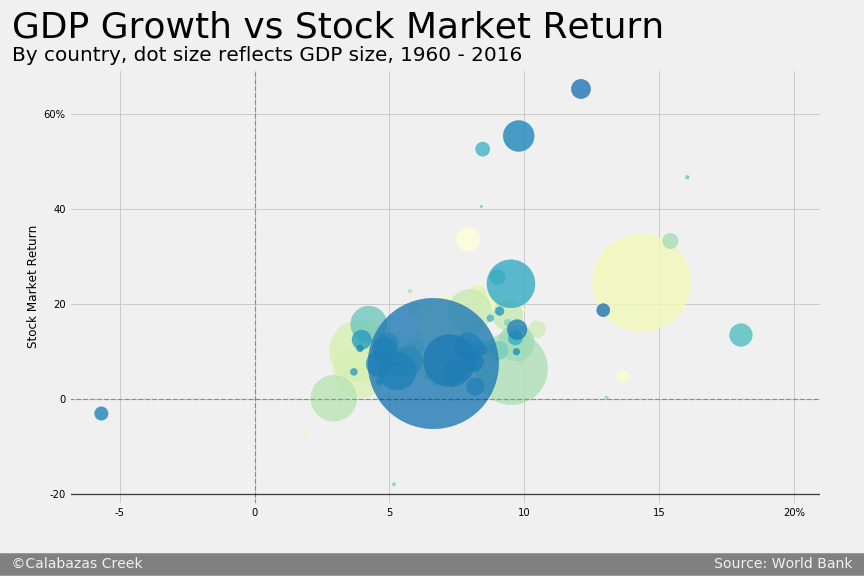

We used World Bank data from 1960 to 2016 across 90 different countries and plotted their average annual GDP Growths and annual Stock Market Returns on a chart to better visualize the potential relationships. Larger dots represent larger GDPs.

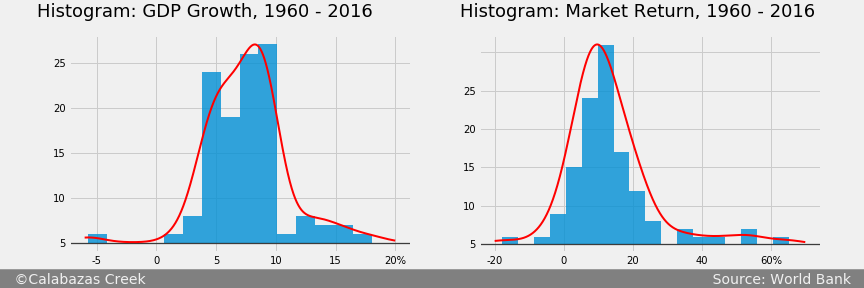

And here’s the distribution of average GDP Growths and average Stock Market Returns for all countries.

After conducting hypothesis testing, we were able to establish that average GDP Growth related to average Stock Market Returns with p value of 0.0007% and R-squared of 45%.

Now, knowing average Stock Market Return is related to average GDP Growth, we then examine each individual country to determine if its Stock Market Return is related to its GDP Growth. After all, if the two variables are not related, then GDP growth, or the expectation of, is not a meaningful reason to allocate into the country.

From the regression results we were only able to confirm that there’s a relationship between GDP Growth and Stock Market Return for 24 countries out of 90.

In addition, for those 24 countries with p-value < 0.05, the coefficient of determination R-squared are all below 67%. Thus, even in the countries where we can establish that Stock Market Return is somewhat related to GDP Growth, GDP Growth does not explain well the variance of Stock Market Return.

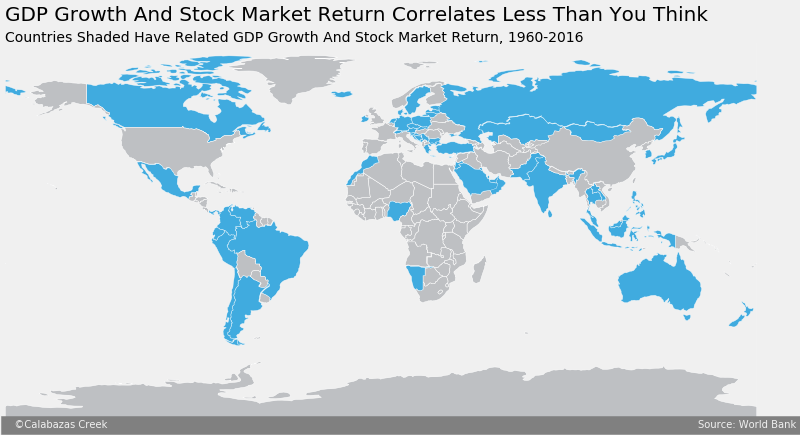

Looking at the list of 24 countries, we find that out of the four BRIC countries, Brazil, India, and Russia are present on the list. The major ASEAN economies such as Singapore, Thailand, Indonesia, Philippines, Malaysia are all on the list as well. Maybe the statistic is not that bad after all for the interesting countries. Here’s a map of all countries with GDP Growth relating to Stock Market Return.

As a caveat, we should note that running regression analysis over over 50 years of time series data has an implicit assumption that all these time series are stationary. This assumption might not be true. For example, the following chart shows China and United States’ change in Stock Market Returns over GDP Growths since 1992 that fluctuates quite a lot between different periods.

Conclusion

“Prediction is very difficult, especially if it’s about the future.”

-Nils Bohr, Nobel laureate in Physics

We have extracted, processed, visualized, and analyzed World Bank’s Stock Market Return and GDP Growth data to determine if investors should use GDP Growth as a factor in allocating capital outside of their home country. While we found that long term GDP Growth and long term Stock Market Return exhibits some relationships, individual country’s GDP Growth and Stock Market Return might not observe the same. Only 24 out of 90 countries with available data exhibits some relationship between GDP Growth and Stock Market Returns. We marked those countries on the map for reference.

Perhaps investors should take cautionary steps next time they use GDP Growth as a rationale for allocating capital to a country.

All data and code can be found on Github.

NO INVESTMENT ADVICE

The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained on our Site constitutes a solicitation, recommendation, endorsement, or offer by Calabazas Creek or any third party service provider to buy or sell any securities or other financial instruments in this or in in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction.